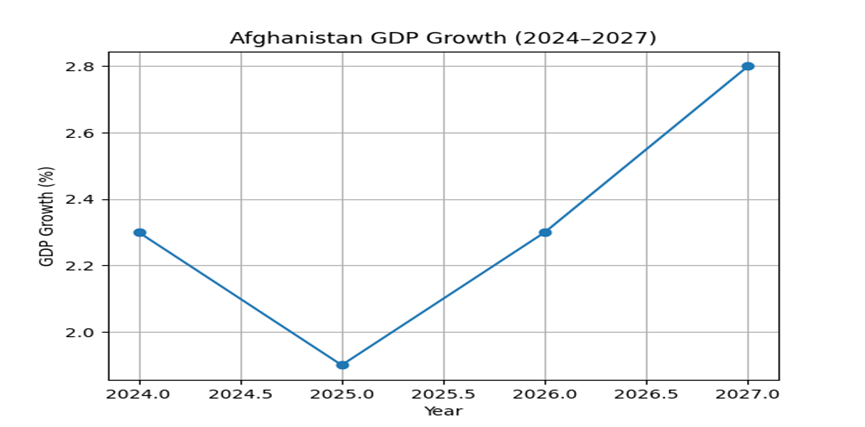

Afghanistan’s economy grew by 1.9% in 2025, slightly lower than 2.3% in 2024, marking the second consecutive year of modest economic recovery since 2021. Private consumption was the main driver of growth, increasing by 15.0%, mainly due to the return of millions of refugees from Iran and Pakistan. Around 1.4 million refugees returned in 2024, while another 2.6 million returned in 2025, causing the population to increase rapidly. Despite this growth in consumption, GDP per capita declined because population growth exceeded economic growth. Public consumption increased by 8.0%, mainly because of higher government spending on security and administration. Investment also recovered, growing by 2.8%, particularly in construction and housing for returning families. However, investment remained relatively low at 17% of GDP.

Agriculture sector was the strongest contributor to economic growth, supported by expanded irrigation networks, improved seed distribution, and favorable weather conditions. Industry and services contributed modestly to growth, while import duties and taxes also supported government revenues to increase. However, reductions in international aid, fiscal constraints, and restrictions on women’s education and employment weakened essential services, with healthcare services declining by 15.2% and education services declining by 9.0%, while broader service sector activity was further constrained as women’s exclusion reduced labor force participation, particularly in urban areas and small enterprises. Although exact estimates vary, UN development reports indicate that the restriction of women’s economic participation contributed to the contraction of thousands of small businesses, especially in retail, education, and NGO linked services, where female employment was previously essential for operations and household income generation.

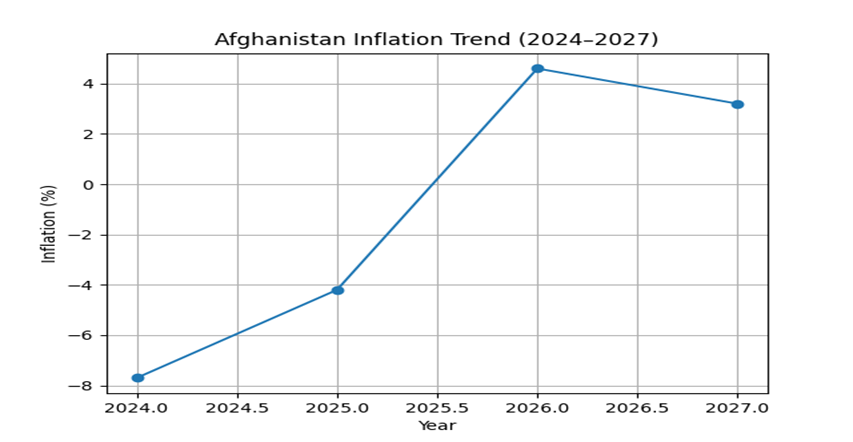

Deflation continued but eased, with inflation improving from -7.7% in 2024 to -4.2% in 2025. Increased domestic demand from returning refugees, supply chain disruptions with Pakistan, and rising housing rents in urban areas mainly in capital city Kabul, contributed to price pressures. Housing demand increased significantly, pushing rents upward by 5.5% year on year.

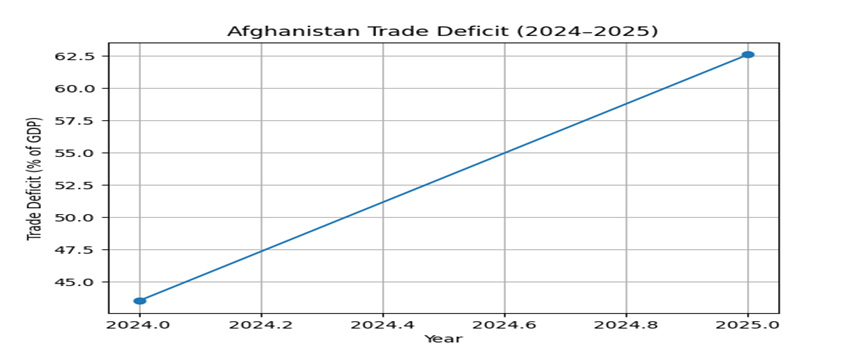

Afghanistan’s trade deficit worsened sharply in 2025, with the merchandise trade deficit rising from 43.5% of GDP to 62.6% of GDP. Imports increased by 36.6%, mainly coming from neighboring and regional trading partners such as Pakistan, Iran, China, and the United Arab Emirates, which supply most of Afghanistan’s food products, fuel, machinery, and manufactured goods. The increase in imports was particularly driven by capital goods, which include machinery, construction equipment, industrial tools, and infrastructure-related inputs used to expand productive capacity. Imports also included fuel, intermediate goods (raw materials and production inputs), and consumer goods.

Afghanistan’s exports remain highly concentrated in a narrow set of primary products, mainly agricultural goods such as dried fruits (especially raisins, almonds, and apricots), fresh and dried vegetables, such as, saffron, medicinal plants, carpets and textiles. Mineral exports (including coal, copper, and gemstones) also contribute but remain unstable due to weak industrial processing capacity and logistical constraints. Despite this, export growth remained modest at 2.1%, while export earnings covered only 15% of imports compared to 21% in 2024. The widening trade deficit is mainly driven by strong import demand linked to population growth, refugee inflows, reconstruction needs, and consumption pressure, combined with weak export diversification, limited industrial capacity, and persistent supply chain disruptions.

The fiscal deficit narrowed from 1.4% of GDP in 2024 to 0.4% of GDP in 2025. Domestic revenues improved significantly because of stronger tax collection and one time asset sales. However, development spending remained very low compared to pre-2021 levels, limiting infrastructure development and public service delivery.

Economic growth is projected to increase 2.3% in 2026, mainly driven by strong domestic consumption, continued refugee inflows, and demand for essential goods and services. However, challenges such as border closures with Pakistan, regional political tensions between Iran and allies (USA and Israel) , higher transaction costs, and limited industrial inputs remain significant. Industry sector is projected to grow by 2.2%, while services may grow by 2.0%. Agriculture sector is expected to grow slowly at 1.7% because of droughts, floods, pests, mismanagement and limited rainfall.

Growth is expected to rise further to 2.8% in 2027, assuming improved regional stability, reopening of trade routes with Pakistan and easing conflict in Iran, reduced transportation costs, and better access to fuel and raw materials. Industrial sector growth could reach around 3.0%, while services may expand by approximately 2.5%. Agriculture may improve slightly to 1.8% if irrigation access and agricultural inputs improve. Inflation is projected to return to 4.6% in 2026 before moderating to 3.2% in 2027. Supply chain disruptions, border closures, and rising food, housing, and transportation costs are expected to remain the main drivers of inflation. However,The fiscal deficit narrowed from 1.4% of GDP in 2024 to 0.4% of GDP in 2025. Domestic revenues improved significantly because of stronger tax collection and one time asset sales. However, development spending remained very low compared to pre-2021 levels, limiting infrastructure development and public service delivery.

Economic growth is projected to increase 2.3% in 2026, mainly driven by strong domestic consumption, continued refugee inflows, and demand for essential goods and services. However, challenges such as border closures with Pakistan, regional political tensions between Iran and allies (USA and Israel) , higher transaction costs, and limited industrial inputs remain significant. Industry sector is projected to grow by 2.2%, while services may grow by 2.0%. Agriculture sector is expected to grow slowly at 1.7% because of droughts, floods, pests, mismanagement and limited rainfall.

Growth is expected to rise further to 2.8% in 2027, assuming improved regional stability, reopening of trade routes with Pakistan and easing conflict in Iran, reduced transportation costs, and better access to fuel and raw materials. Industrial sector growth could reach around 3.0%, while services may expand by approximately 2.5%. Agriculture may improve slightly to 1.8% if irrigation access and agricultural inputs improve. Inflation is projected to return to 4.6% in 2026 before moderating to 3.2% in 2027. Supply chain disruptions, border closures, and rising food, housing, and transportation costs are expected to remain the main drivers of inflation. However,The fiscal deficit narrowed from 1.4% of GDP in 2024 to 0.4% of GDP in 2025. Domestic revenues improved significantly because of stronger tax collection and one time asset sales. However, development spending remained very low compared to pre-2021 levels, limiting infrastructure development and public service delivery.

Economic growth is projected to increase 2.3% in 2026, mainly driven by strong domestic consumption, continued refugee inflows, and demand for essential goods and services. However, challenges such as border closures with Pakistan, regional political tensions between Iran and allies (USA and Israel) , higher transaction costs, and limited industrial inputs remain significant. Industry sector is projected to grow by 2.2%, while services may grow by 2.0%. Agriculture sector is expected to grow slowly at 1.7% because of droughts, floods, pests, mismanagement and limited rainfall.

Growth is expected to rise further to 2.8% in 2027, assuming improved regional stability, reopening of trade routes with Pakistan and easing conflict in Iran, reduced transportation costs, and better access to fuel and raw materials. Industrial sector growth could reach around 3.0%, while services may expand by approximately 2.5%. Agriculture may improve slightly to 1.8% if irrigation access and agricultural inputs improve. Inflation is projected to return to 4.6% in 2026 before moderating to 3.2% in 2027. Supply chain disruptions, border closures, and rising food, housing, and transportation costs are expected to remain the main drivers of inflation. However, a strong Afghani currency and stable global commodity prices may help reduce inflationary pressure over time.

The banking sector has shown slight improvement, with lending in local currency increasing by 7.0% and deposits increasing by 7.6%. Despite this, banks sector remain highly cautious because of weak profitability, nonperforming loans, payment restrictions, and uncertainty surrounding Islamic finance regulations. As a result, the banking sector is still unable to strongly support economic growth.

Afghanistan’s economic outlook faces significant risks, including regional political instability, continued border closures, rising energy prices, supply chain disruptions, climate related shocks, and reduced international aid. These risks could increase inflation, reduce economic growth, worsen unemployment, and place further pressure on public services.

Between 2024 and 2025, around 4 million refugees returned to Afghanistan from Iran and Pakistan. Most returnees face housing shortages, unemployment, limited access to healthcare, education, lack of documentation and financial resources. Only 11% of returnees reportedly secured full time employment. Key policy priorities include job creation programs, government backed skills training, support for women led households, home-based businesses for women, microfinance, small business grants, financial literacy programs, expansion of mobile banking such as AziPay mobile wallet and microfinance institutions. Community based reintegration programs are also essential to maintain social cohesion, reduce tensions with host communities, and promote long-term economic integration. In nutshell, the stated analysis illustrates, that Afghanistan’s economic recovery remains fragile and highly dependent on regional stability, trade access, and the effective management of returning refugees. While refugee inflows have increased domestic consumption and supported short-term economic activity, they have also placed heavy pressure on employment, housing, healthcare, and public services. This reflects the economic principle that rapid population growth without sufficient productive capacity can reduce GDP per capita and increase inflationary pressures. In the short run, the government and international organizations should focus on cash-for-work programs, vocational training, housing support, and small-business assistance to help returnees reintegrate into the economy. In the long run, refugee returnees could become an important source of labor, entrepreneurship, and human capital; if Afghanistan government invests in education, infrastructure, agriculture, financial inclusion, and regional trade connectivity. Therefore, Afghanistan’s future economic stability is largely depend on its ability to transform the refugee return challenge into an opportunity for sustainable economic development, social cohesion, and long-term economic resilience.

References

Asian Development Bank. (2025). Asian development outlook 2025: Afghanistan chapter. Asian Development Bank. Da Afghanistan Bank. (2025). Banking and monetary sector updates 2024–2025. Da Afghanistan Bank. International Monetary Fund. (2025). Regional economic outlook: Middle East and Central Asia. International Monetary Fund. International Organization for Migration. (2025). Afghanistan returnee situation reports 2024–2025. International Organization for Migration. United Nations Development Programme. (2025). Afghanistan socio-economic outlook 2025. United Nations Development Programme. United Nations High Commissioner for Refugees. (2025). Afghanistan returnee and reintegration reports 2024–2025. United Nations High Commissioner for Refugees. World Bank. (2025). Afghanistan development update. World Bank.

By: Mohammad Ameen Waheb & Obaidurahman Niazi